July Monthly Wrap - saying no to an early stage investment in FB, GOOG and TSLA, match fixing and how ethical is Visa?

Monthly Wrap

Every month I share an update on this newsletter and a summary of what I’ve read, seen or heard that I’ve found interesting. Expect the format to evolve over time, as well as what’s included. If you have any feedback, please hit me up! If you missed the June Monthly Wrap, you can find that here.

If you are not already you can follow me on Twitter here (@tlginvestor).

Thanks for reading The Long Game! Join over 300 like minded, curious and intelligent individuals to receive new posts and support my work.

The Long Game Update

I’ve not written as much as I’d like for the last couple of months. There are a couple of contributing factors being work has been extremely busy (with a decent chunk of travel) and I’m spending more time thinking about the current macro environment and what this means for investing - but more on that topic later. I am currently working on a 3 seperate company deep dives, which I anticipate at least one will be ready at some point in the next few weeks, so I’m hoping to publish something company specific in August, work load permitting.

I also clearly need some help with social media, my plan to tweet more regularly to promote the newsletter failed miserably in July - here’s hoping for a more productive twitter handle in August! If you’re not already feel free to give me a follow here (or if you like what you read each month - share this article).

The pseudo hedge fund? Why I am uninvested and continue to hoard cash.

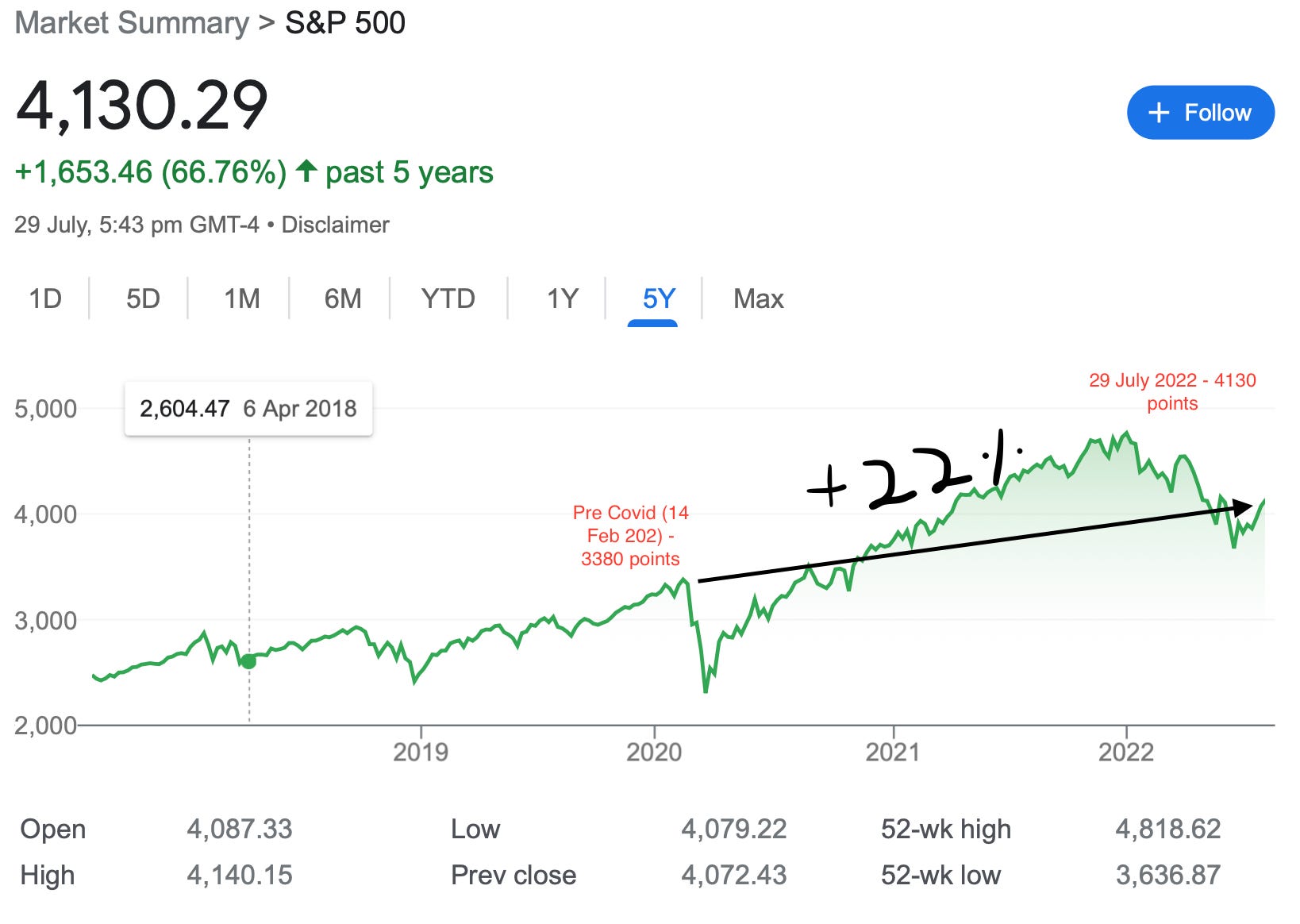

Last month I said valuations have cooled to pre-covid levels, however I note this comment was specifically referring to SaaS / Tech multiples (most but not all of the businesses I tend to invest in). A colleague of mine recently made an interesting point which I share below via illustration. It just doesn’t feel right that the S&P500 is 22% higher than where it was pre covid, despite the current macro environment.

I still think the market hasn’t fully priced in continued interest rate hikes and geo political risk / unrest (de globalisation is a concept I’ve been thinking about recently). I continue to maintain a watch list of ~15 stocks, and may opportunistically initiate a position where I see a particularly compelling entry point. I’m most excited about the potential to buy high quality infrastructure SaaS businesses at reasonable prices (still no names disclosed yet!).

What I have been reading, watching and listening to

Every month I will share a selection of things that I’ve found interesting. Here’s what caught my attention in July:

The Bessemer anti portfolio – Bessemer Venture Partners a top tier venture firm out of the valley with additional offices in India and Israel. They’ve invested in some amazing companies including Twillio, Shopify and Pinterest (to name a few). Venture Capitalists arent known for their humility, and it’s not often you’ll hear a Venture Capitalist openly admit to missing an iconic company. In this piece Bessemer is openly paying homage to some of the great companies they decided not to invest in and providing the reasons for not investing. Some times it was deciding between which meeting to take with a coin toss due to a flight delay ( passing on SNAP 0.00%↑ ) or an “outrageously expensive” pre IPO valuation ( passing on AAPL 0.00%↑ at $60m). The full list and reasons for declining makes for some good reading (with a few laughs). Google, Tesla and Facebook stood out for me:

Google (GOOG 0.00%↑ ) - David Cowan’s college friend rented her garage to Sergey and Larry for their first year. In 1999 and 2000 she tried to introduce Cowan to “these two really smart Stanford students writing a search engine.” Students? A new search engine? In the most important moment ever for Bessemer’s anti-portfolio, Cowan asked her, “How can I get out of this house without going anywhere near your garage?”

Tesla (TSLA 0.00%↑) - In 2006 Byron Deeter met the team and test-drove a roadster. He put a deposit on the car, but passed on the negative margin company telling his partners, "It's a win-win. I get a great car and some other VC pays for it!" The company passed $30B in market cap in 2014. Byron paid full price for his Model X.

Facebook ( META 0.00%↑ ) - Jeremy Levine spent a weekend at a corporate retreat in the summer of 2004 dodging persistent Harvard undergrad Eduardo Saverin's rabid pitch. Finally, cornered in a lunch line, Jeremy delivered some sage advice, "Kid, haven't you heard of Friendster? Move on. It's over!"

Bessemer Investment Memo’s - While we are on the topic of Bessemer Venture Partners, they have also published their early investment memo’s in a number of their iconic investments. This is remarkable. VC’s typically guard their memo’s closely - so Bessemer to share its early stage memo’s is unusual. For those of you who are looking at investing in some of these companies since they have gone public, its interesting to see how a top tier early stage VC underwrote at an earlier rounds when the company was only generating a fraction of revenue (or none at all!) or perhaps had a product road map that was quite nascent / not clearly defined. I loved reading all of them but Toast ( TOST 0.00%↑ ), Twillio ( TWLO 0.00%↑ ) , Rocketlab ( RKLB 0.00%↑ ) and Pinterest ( PINS 0.00%↑ ) were a few I found super interesting!

Calculating Return on Invested Capital - A friend of mine sent me this paper (from back in 2014) and found it to be a concise but comprehensive overview on calculating the ROIC metric. The paper completed by a couple of folks at Credit Suisse provides a practical guide (with case studies) on how to calculate this metric while still considering various nuances associated with different accounting items and the metric. ROIC one of the most important calculations that investors use to asses the the capital allocation ability of a company, and this paper is something you should refer back to as you do analysis.

A core test of success for a business is whether one dollar invested in the company generates value of more than one dollar in the marketplace. Warren Buffett, the chairman and chief executive officer of Berkshire Hathaway, calls this the $1 test.1 Logically, this occurs only when a business earns a return on investment in excess of the opportunity cost of capital.

Here’s an extremely simple example. Say a company invests $1,000 in a new factory and estimates that the cost of capital is 10 percent. Were the factory to generate $80 in after-tax earnings into perpetuity, the market value of the factory would be $800 ($80/.10) and the investment would fail the $1 test. Earnings of $120 would create value of $1,200 ($120/.10), hence passing the $1 test. As companies announce investments such as acquisitions or capital expenditures, the market renders its judgment as to whether the investments add or detract from value.

The fixer, the cheat and the corruption crisis in global tennis - not an investing related article but a really interesting piece of journalism all the same. While I find the concept of match fixing abhorrent, its hard not to feel for some of these fringe players on the professional tennis circuit. The clear issue here is that to make a decent living (when you consider expenses particularly travel and medical) a tennis player really needs to be a top 100 player, the remainder of players end up struggling to make ends meet.

He told me he’d agreed to speak with me because he wanted to highlight the poor pay most professional tennis players receive, compared with sports like football or golf. Most struggle to break even, which makes them vulnerable to corruption. (His page on the ATP website lists Kicker as having career winnings totalling $946,683, with $53,837 this year.)

For as long as there’s a financial incentive and an opportunity to fix matches, there will probably be stories like Kicker’s. And although the ITF has increased prize money across lower-level events, the game is still able to support just a tiny number of those who play professionally. The ITF has been implementing a ranking point structure designed to keep the best players moving up and, theoretically, earning more.

It is also reviewing whether more events can offer hospitality, and is collaborating with the sport’s other governing bodies to reduce players’ travel expenses by scheduling a block of tiered tournaments in the same region. The ITF hopes to eventually enable the top 750 men and 750 women to earn a living from the sport, though it cannot say by when.

Tweet of the Month

Every month I will share a Tweet I came across that I found interesting. For July, it’s this tweet thread from Bill Ackman attacking Visa / V 0.00%↑ for providing the payment infrastructure to facilitate some truly horrific and deplorable activity. ESG and responsible investing is becoming more prominent as investors become more focussed that the companies they invest in are adding value not just economically but are also ethical, and Ackman makes a pretty compelling argument about Visa’s responsibility in these situations, specifically calling out Visa’s CEO’s Alfred Kelly, who as Ackerman puts it “waxes eloquent in his annual letter about Visa’s ‘noble’ purpose, commitment to an ‘inclusive economy’ and ‘economic opportunity for all.’ He then trumpets the hiring of a Chief Diversity Officer in May 2021 reporting directly to him.” I wonder how many “ethical” portfolio’s have V 0.00%↑ in it?

Stay patient, focussed and rational.

TLG