Cvent (potentially) a quiet compounder in the making

Investment notes

Disclaimer: The below does not constitute investment advice. Please do your own research or obtain your own advice. The views presented are our own. We do not own CVT shares at the current time, but are watching them closely. We will update this disclosure if either of us buy the stock.

Note: This article on Cvent is co-authored by Young Money Capital and The Long Game. If you’re not already, feel free to subscribe to our Substack’s.

Overview

As a technology company founded in 1999, Cvent feels like an anomaly for a tech company that recently went public via a SPAC. The company is led by founder Reggie Aggarwal and provides a SaaS-based solution to assist event planners to organize meetings and events (including marketing). The business, which is based in Tyson VA, has over 4000 employees and has been able to navigate the dot com bubble (coming close to bankruptcy), GFC, and Covid 19 disruptions during its 20-year life. The company was first listed in 2013 before it was taken private by Vista Equity Partners. Vista, who at the time owned Cvent’s largest competitor, Lanyard, merged the two companies. The combined company tripled Cvent’s revenues and doubled its headcount. Cvent also invested heavily in R&D to rebuild its technology stack. While when COVID hit, Cvent didn’t have a virtual event offering, the company was able to launch Virtual Attendee Hub, its platform for virtual events in 2020, and pivot the company relatively quickly (less than 5 months).

Cvent has 2 platforms it offers customers:

Event Cloud (70% of revenues): Cvent’s flagship product which helps planners optimize engagement throughout the entire event life cycle, including speaker management, lead conversion, and post-event insights.

Hospitality cloud (30% revenues): a marketplace to connect planners to hotels and venues

The company also has a strong track record with acquisitions, having made ~16 tuck-in acquisitions in the last decade to augment capability. The vast majority of these have been small tuck-ins with only one being more than $100m.

Investment thesis - what do we need to believe to compound capital at 20%+?

The investment thesis here is that the company is the clear market leader in providing SaaS-based solutions to the event management industry that is trading at a very reasonable valuation (~4x NTM revenues). Cvent has a meaningful opportunity to expand internationally and upsell existing customers. Today only ~13% of revenues are derived internationally and the majority of customers only use one Event Cloud product. Additionally approximately ~12% of customers have purchased the virtual module, meaning there is material upsell potential. Almost half of the ~12% of customers who purchased the virtual module, doubled their spending (given the per user pricing), suggesting significant whitespace within its customer base. We have set out what investors need to believe to achieve a 20% IRR in the valuation section of this paper.

Industry trends: Hybrid Events are the new normal

The Covid 19 pandemic stopped all in-person events and Cvent which traditionally derived all (~95%) of its revenue and was forced to pivot quickly to offer virtual event capability. It took the company less than 5 months to launch the Virtual Attendee Hub for virtual events. The increase in digitization of the event industry means that virtual events are likely to become more prominent. While some event types will always require a physical presence for product demonstrations and networking, virtual events allow organizations to engage with a larger audience more efficiently, hosting more events at a lower cost (given the digital infrastructure) without sacrificing marketing return on investments. Expert calls suggest that post-pandemic, several companies have already indicated that they expect to hold hybrid events, meaning they can attract a larger number of attendees than a person-only event. The emergence of hybrid and virtual events dramatically increases the TAM for the company to ~$30bn as estimated by Frost and Sullivan ($26bn for Event Cloud and $4bn for Hospitality Cloud). Cvent’s product offering means it capitalizes on the increased digitization and the rise of virtual events, while still servicing its traditional in-person event customers.

Why does Cvent win?

There are three reasons why management believes Cvent is the leader in the space - network effects, contracts/pricing model, and best product. While the product advantage (so far) is clearer, the network effects are less so.

Network effects

Cvent’s management claims they have network effects that provide their company with a moat. They describe their network effects as “a global marketplace for both sides of the events ecosystem, CSN (Cvent Supplier Network) is a critical external lead generation channel for event and group meetings business.” They have over 290,000 venues on their marketplace and 11,000 Cvent cloud customers.

This marketplace allows customers to search for the right venue for their event and standardize the RFP saving time. While there is a network effect, some people question how strong it is currently and how strong it will be in the long term. Venues can be listed on multiple event cloud platforms and customers could subscribe to multiple event planning platforms which defeat the purpose of a network in a way. Industry experts say that it is not that hard to switch from one provider to another. The best way Cvent locks in their network is through their pricing model and long-term contracts and ensuring they remain the most user-friendly platform.

Go to market/pricing model

Cvent has an inside and field sales team, and has been able to ramp reps efficiently with sales per rep exceeding pre pandemic levels. The company leverages almost 2000 employees (most of which are in marketing) in India as part of its sales process to capture and convert the bulk of its inbound leads.

Some customers use multiple different event planners depending on the need for the event. Cvent tries to lock their customers in with contracts. While Cvent calls its revenue model subscription-based, which implies high switching costs, it is also important to note it is a partially usage-based model. The addition of virtual/hybrid events has resulted in over half of customers (who have added the virtual model) doubling their spending. “Subscription revenue is driven primarily by the number of registrations purchased and the number and complexity of mobile applications, onsite events, and virtual events purchased in addition to additional modules that enhance the functionality of the software solution.”

Cvent’s pricing model is different for its Event and Hospital Cloud offerings.

Event Cloud: Cvent charges an annual subscription fee (up to $20k per year) and anywhere between $2 and $6 per registrant at an event, providing volume discounts for scale. The virtual module charges a $2k per year annual subscription fee with a similar per registrant fee. Customers are also charged for add-on solutions not included in the base subscription fee.

Hospitality cloud: the company uses a subscription plus advertising model, where customers pay a flat fee to be on the platform. Subscription fees charge predominantly reflect the size of the premises. Customers can pay additional advertising fees to promote their venues in addition to this. Subscription fees are approaching ~50% of all hospitality cloud revenues, and reduces the volatility associated with ad revenues. The upfront fees and volume-based discounts encourage customers to use only one platform.

Product Advantage

Cvent does have a strong product advantage. Cvent is known for its strong customer support team, great check-in systems, and its ease of use. The drawbacks are that Cvent is more expensive than competitors like Aventri and Hoppin and they have a less customizable workflow. Cvent’s product advantage could be durable due to its management team. According to an industry expert, Cvent’s product was very weak in 2019, but has rapidly improved and has become the best product.

The product advantage is evidenced in some of the key customers Cvent has acquired. They have onboarded 23 of the top 25 pharmaceutical companies and 6 of 8 ivy league schools. The question is how long can Cvent maintain its product advantage.

It’s possible that Cvent could use its product advantage to build a strong competitive advantage. This would entail them gaining enough market share that venues need to use them for planning events, instead of seeing them as an additional revenue stream. Cvent then could leverage its scale with venues on behalf of customers and pass cost advantages onto them creating a flywheel and having venues pay for search engine optimization on Cvent’s platform. At this point, Cvent has a long way to go to build that competitive advantage.

Where could we be wrong?

Overall we see the following risks with an investment in Cvent.

Competitive market environment: The competitive environment which CVENT plays is unique in that several competitors are servicing the event cloud space. Hoppin represents the most advanced and well-funded of these. To date, Hoppin has raised ~$1bn from VC backers including A16Z, General Catalyst, Tiger, and Altimeter (amongst others). The business has quickly grown, with public sources indicating the business has already reached $65m of ARR (combination of organic and inorganic growth). Hoppin has been highly acquisitive buying Boomset and StreamYard to augment its product capability. Other players in the space include Aventri, Bissabo, and On24. Additionally, in the early stages of the pandemic, several virtual meeting companies emerged. To date, most of these only offer a virtual offering only and aren’t as customizable or feature-rich as Cvent, which allows organizations to engage directly with their customers and vice versa. Additionally while Zoom currently only plays in the video conferencing space, there is a risk that Zoom could start rolling features to compete with Cvent, and enter the event management space. While Zoom’s product roadmap in events is not known, given Zoom was a large investor in Cvent’s SPAC, there is some alignment between both companies.

COVID continues to persist and new variants may curtail in-person person events: In its Q1 earnings call management noted that Omicron was creating a challenging growth environment. If new variants emerge this is likely to slow down customer appetite for in-person and hybrid events. While the company has a strong virtual offering, the hybrid and in-person events are where Cvent has the strongest competitive advantage and stands to take market share from its competitors. Given the world (except China) has moved past broad-based lockdowns and international travel has opened up, this risk is likely to only play out if there is an extreme variant that emerges.

Execution risk to capture international and upsell opportunity: Part of the thesis for Cvent is the meaningful opportunity to expand internationally and upsell existing customers. Today only ~13% of revenues a derived internationally and the majority of customers only use one Event Cloud product. Additionally approximately ~12% of customers have purchased the virtual module, suggesting there is material upsell potential. To capture this opportunity, the company will need to invest substantially in its sales and marketing capacity and will require strong execution from management to ensure that reps ramp efficiently and effectively.

Macro uncertainty, near-term recession risk: in addition to COVID, rising interest rates, the continued risk of a recession, and the volatility in public markets for SaaS multiples, means that the company’s stock price will likely be volatile for the short to medium term. A prolonged recession will likely impact Cvent as organizations move to cut discretionary spending and marketing budgets. While several economists have noted a recession is likely, most believe it will be short-lived and reasonably shallow.

Thoughts on Management, its Capital Allocation ability, and alignment

Cvent is led by CEO and Cofounder Reggie Aggarwal who is supported by a high-quality management team. Reggie has led the business for 20 years through various macroeconomic cycles working with Private Equity and in the public markets. Informal, off-sheet references have suggested that Reggie is extremely well regarded.

Cvent successfully managed the Covid crisis where they were unable to have in-person events and developed a hybrid event platform within 5 months of the pandemic Customers say their platform was weak in 2019 but has improved to be the best option currently. 91% of Cvent attendees claimed the platform was easy to use. This is a testament to management's ability to navigate difficult situations and create a top product.

Cvent’s management team is primarily compensated with stock options. Cvent describes it as a “pay-for-performance approach (that) aligns the interests of our named executive officers who provide services to us with those of our stockholders.” The incentive plan is recently negotiated after Dragoneer de-spaced Cvent.

Source: CVT SEC Filings

So far, the majority of Cvent’s cash from operating activities has been used to invest in software development and build up its cash position. Of the $102 million that Cvent spent in investing activities over the past two years, 82 million were for capitalizing software development costs. Cvent also made two small acquisitions and capitalized a few other smaller expenses.

Cvent has also been building up its cash position from the covid lows of $65.3 million. Unfortunately, it is unclear what Cvent is building its cash position for.

Source: Koyfin

Cvent does not currently offer a dividend and has had a 1-4% dilution since their SPAC.

Valuation

Cvent currently trades at ~4.3x NTM revenues. We have set out ‘what you need to believe’ for a 20% IRR on Cvent below. Base case assumptions are set out below:

Revenue growth of ~20%

EBITDA margins growing to ~29% as the business benefits from scale over the near term. Management has guided long-term margins of 35% to 40%. While we assume that the R&D as a percentage of revenue will decline, we have fully loaded Sales and Marketing / G&A to support our revenue growth assumptions.

An exit EBITDA multiple of 15x.

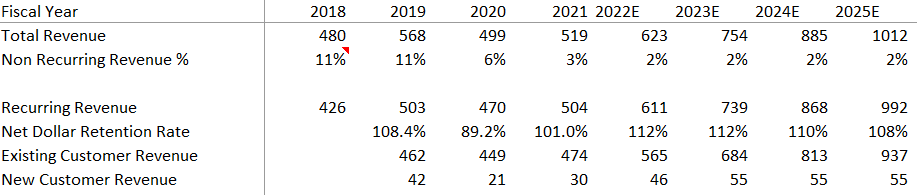

Cvent’s key revenue driver is its net dollar retention rate. It fell off during Covid as companies cancelled in person events. Last quarter, Cvent had a 109% net dollar retention rate. In order for Cvent to return a 20% IRR, an investor needs to believe that Cvent can have a ~112% net dollar retention rate and that it is sustainable. Cvent’s management guidance for revenue is in line with the below projections.

Revenue Drivers

Source: Author, Historical Data from Koyfin

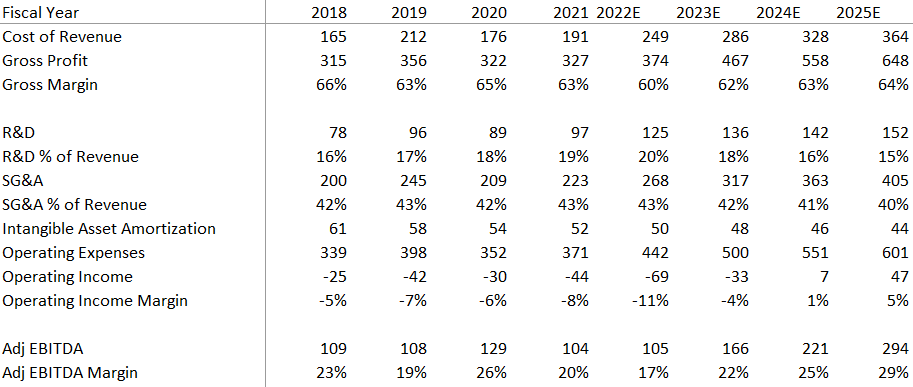

As Cvent ramps revenue, it will need to show economies of scale to achieve a 20% IRR. Cvent expenses as a percentage of revenue in the below projections are still below management’s long-term goals. Its adjusted EBITDA margin is significantly higher than the operating income margin due to depreciation and stock-based compensation. Stock-based compensation should be taken out as it will be compensated for later in the diluted shares outstanding line item.

Expenses

Source: Author, Historical Data from Koyfin

Cvent will need to continue to limit its dilution with stock repurchases to achieve the 20% IRR. They can have some multiple compression, but they will still need to have a healthy exit multiple of 15. It is up to the reader to decide whether these assumptions are realistic.

Exit Multiples

Source: Author, Historical Data from Koyfin

Wrap up

One of the great things about investing is that two people can have the same set of facts but reach different conclusions - it's what makes investing what it is. Here are some wrap thoughts from each of us on Cvent as an opportunity.

The Long Game’s thoughts

I am more convinced of the underlying network effects of the Cvent platform than my friend YM Capital. The under-appreciated (power) of Cvents product, in my view, is that they are just as user-friendly for event planners as it is for venues, and it enables seamless collaboration between both sides of the event, and therein lies the network effect. I think the current valuation represents a very attractive entry point to buy a market leader led by an extremely high quality and well-seasoned CEO, Reggie Aggarwal. In my view, the market is punishing the company for going public via SPAC, and it’s been associated with several lower-quality companies that were able to go public when they probably shouldn't have. I think Cvent is one of those companies that can quietly compound revenues at 20% before generating FCF margins of 30% as a mature business in the longer term. I think businesses with this sort of profile, typically trade at 6-8x revenues through the cycle, so in addition to operational growth, the possibility for multiple expansion also exists. While YM is less convinced on the forecast assumptions for a 20% IRR - mine is that they are not heroic, and below management’s long term operating guidance.

Young Money Capital’s thoughts

I agree with The Long Game Investor that Cvent is the industry leader and will benefit from a shift to more hybrid events. I am more skeptical of the network effects. The comment that spooked me is an expert discussed how he uses multiple event planning platforms, which implies that the network effects are weak. Despite my skepticism about the network effects, I do believe Cvent is attractively priced here, but I think the assumptions to get a 20% IRR are a bit aggressive. Product advantages can last for a long time when managed by a great management team and Cvent is benefitting from a significant tailwind in the shift to hybrid events. Their increasing NRR supports that thesis and as long as they stay the industry leader, they should be able to expand margins and provide an attractive return for investors.

One final thing from The Long Game. For any readers looking for a US based analyst who is pretty early in their career, I’d strongly encourage you to connect with YMC. I’ve gotten to know him as we’ve worked through this piece, and I’ve found him to be very bright, intellectually curious and insightful. Feel free to reach out to him directly, or I can make an intro - having worked with him closely over the last couple of weeks I promise you’ll enjoy the discussion.

| A guest post by

|

Great read! Out of the two business segments, which one do you guys think will be the greater growth driver?